Yahoo Finance

Yahoo Finance Posthaste: This missed CPP opportunity is costing Canadians thousands, says report

Most Canadians — in fact nine out of 10 — say the Canada Pension Plan is an important source of their retirement income and six out of 10 say it’s essential and they can’t do without it.

Yet according to a new report from the National Institute on Aging, the vast majority are not making the most of the government retirement plan.

Canadians can start claiming at age 60, but the earlier you start, the lower your payments. You can defer your pension until age 70 and the longer you wait the higher payments climb.

According to the report, waiting until 70 would more than double your monthly pension than if you start collecting CPP at age 60.

A Canadian with median CPP income and average life expectancy is losing out on more than $100,000 worth of income, in current dollars, by taking CPP at age 60 rather than 70, said Bonnie-Jeanne MacDonald, the NIA’s director of financial security research and head author of the report.

Yet nine out of 10 Canadians opt to take these benefits by age 65 or earlier.

Claiming CPP is easy, but deciding when to claim is not, said MacDonald. Despite being one of the most important financial decisions Canadians will make, two out of five CPP recipients say they didn’t consult anyone or any resources before making it.

“This is a once-in-a-lifetime, high-stakes financial decision, and its complexity leads people to make choices that are not in their best interest,” said MacDonald. “By claiming too early, recipients are reducing the lifetime income security that they report to want and will most likely need.”

The stakes have never been higher. More than a thousand Canadian baby boomers are making the claiming decision every day, and while retirement costs are increasing, sources of secure long-term retirement financing are shrinking, the study says.

Since the 1970s, access to defined benefit pensions has decreased in the private sector from three in 10 to one in 10 today.

And while two-thirds of Canadians hold registered retirement savings, such as RRSPs or defined contribution plans, the median balance is only $100,000.

“This level of savings is frighteningly inadequate,” said MacDonald.

“In the new reality of longer lives, less available family support and growing fiscal pressures on health and social programs for older adults, it is critical to use the little retirement savings held by Canada’s substantial retiring population as efficiently as possible.”

Deferring CPP isn’t for everyone and the report stresses it is not meant as personal financial advice. For retirees facing financial hardship or ill health that means shorter life expectancy, claiming CPP at 60 is a rational decision.

Nor is deferring without controversy. Some argue that waiting just means you are getting higher payments for a shorter period of time.

But what the report argues is that it makes more financial sense for retirees to use their less secure RRSP savings first to bridge the gap until age 70, allowing a higher and more secure income to kick in.

“Drawing on personal savings in early retirement as an income bridge to a higher delayed CPP/QPP benefit is a financially advantageous investment strategy to generate greater secure lifetime income,” said MacDonald.

An earlier NIA study found that four out of five Canadians with RRSPs or RRIFs would get more lifetime income by using a portion of these savings to bridge the gap until 70 than spreading them out over the span of their retirement.

The report also argues that most Canadians can afford it. Using a Statistics Canada simulation model, the NIA calculated that more than half of 60-year-old Canadians could have delayed their CPP and 27 per cent could have waited until 70 by using only a portion of their private savings.

Even $100,000 in RRSPs, though not much over the entirety of a retirement, is enough to bridge the income gap, said MacDonald.

Why Canadians are not waiting spans a range of reasons, from ignorance of the rules to bias among financial advisers to human psychology. A poll in 2018 by the federal government found that two thirds of Canadians didn’t know that waiting to claim CPP would increase their payments. A common fear is that the government pension plan will run out of money.

The purpose of the paper and a series of reports to come is to shift the paradigm and help Canadians make more evidence-based and unbiased CPP claiming decisions, said MacDonald.

And behaviour is slowly changing. Over the past 10 years there has been a move away from claiming CPP at age 60, but it has been gradual and only one in 10 wait past age 65, she said.

Sign up here to get Posthaste delivered straight to your inbox.

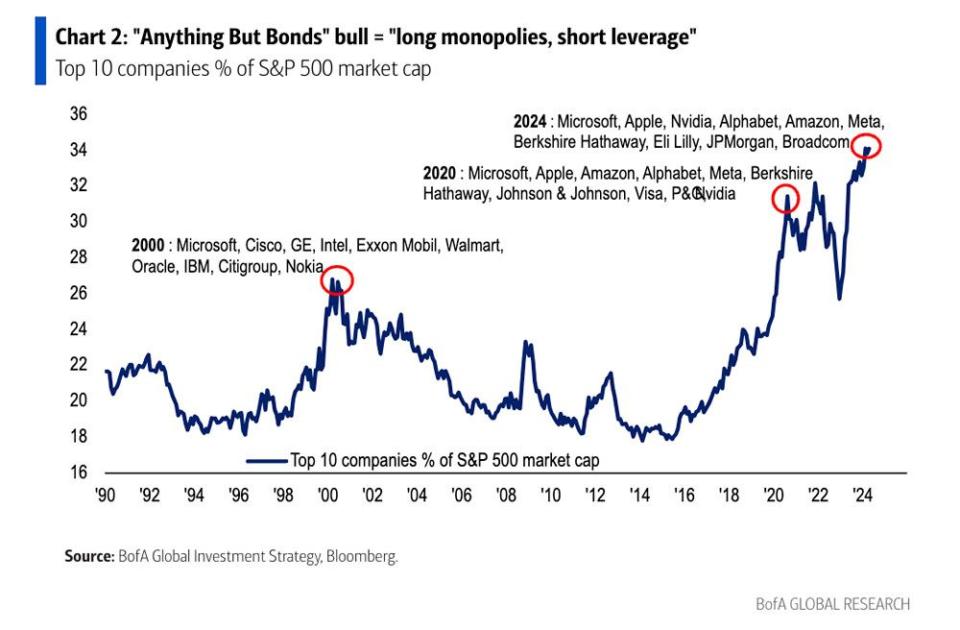

The Magnificent Seven ride again. April has been a bumpy month for markets but this group, which includes Nvidia Corp., Apple Inc. and Amazon.com Inc., is still running ahead of the pack.

The 10 largest U.S. stocks combined now represent a record 34 per cent of the S&P 500 Index market capitalization, says Bank of America strategists, who bring us today’s chart.

The strategists led by Michael Hartnett say the leadership of these mega-caps will remain until real 10-year yields rise to about 3 per cent or “higher yields combine with higher credit spreads to threaten recession.”

Earnings: Cargojet Inc, Gibson Energy Inc, Domino’s Pizza Inc, Revvity Inc, Franklin Resources Inc, Paramount Global

A whopping 25 per cent of Canadians say they’ll miss the April 30 tax-filing deadline entirely, thereby risking a late-filing penalty and arrears interest on any tax owing. That’s just one reason why tax expert Jamie Golombek says it’s important to do some tax planning year-round, not just in the last few days of April. Get some last-minute tips here.

Are you worried about having enough for retirement? Do you need to adjust your portfolio? Are you wondering how to make ends meet? Drop us a line at aholloway@postmedia.com with your contact info and the general gist of your problem and we’ll try to find some experts to help you out while writing a Family Finance story about it (we’ll keep your name out of it, of course). If you have a simpler question, the crack team at FP Answers led by Julie Cazzin or one of our columnists can give it a shot.

McLister on Mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Read them here

Today’s Posthaste was written by Pamela Heaven with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.